The Registered Disability Savings Plan (RDSP) is a special savings plan designed for people with disabilities. It’s the first of its kind in the world. It is like a Registered Retirement Savings Plan (RRSP) but with some big differences.

By opening an RDSP, you can get free money from the government. This money can be a big help for you or your family member to save for the future.

What is a Registered Disability Savings Plan (RDSP)?

If you or your family member qualifies for the Disability Tax Credit (DTC), you can open a Government of Canada Registered Disability Savings Plan (RDSP). We know that the DTC can be hard to apply for, but having the DTC lets you take advantage of this program too.

An RDSP helps people with disabilities save money for the future. You or your family member may be able to get free money from the government in the form of matching grants and bonds. The amount of money depends on how much your or your family income is. The RDSP can be a useful tool for the financial security of people with intellectual disabilities and their families.

Here are some basics about the RDSP:

- The RDSP is designed as a retirement plan, which means that the money usually stays in the account until you (or your family member) turns 60. While the money is in the account, it can be invested so it continues to make money and grow.

- You can put in up to $200,000 of your own money, but anyone can put money into your RDSP for you. This means that you, your family, friends, or anyone else that you give permission can put money into your RDSP.

- For every $1 that is put in your RDSP, the federal government could match with up to $3 depending on family income.

- For people with low incomes, the government will put in up to $1000 per year and up to $20,000 in total for you. This money will go into the RDSP automatically just by having it open.

- Your provincial/territorial disability funding or income assistance and benefits won’t be affected or reduced because of your RDSP or any money you take out of it. You get to keep all your benefits that you have today. This is an important part of the program.

- Like an RRSP, an RDSP is also tax deferred. This means that any money you have in the plan will keep growing without having to pay any taxes (money to the government) until you take money out.

Who is eligible for the RDSP?

To have an RDSP, you need to:

- Qualify for the Disability Tax Credit (DTC)

- Have a valid Social Insurance Number (SIN #)

- Be a Canadian resident

- Be 59 years old or less

Banks and financial advisors can help you open your RDSP. It’s best to open an RDSP as soon as possible so you can take advantage of the maximum amount of government and personal contributions. Parents of a child with a disability can even open an RDSP on their behalf.

When can you take the money out?

RDSPs save money for the future. They are meant to provide money for people with disabilities at age 60 so they can buy the things they need to live.

Once you turn 60, you can take money out of your RDSP without any penalties (this means you won’t have to pay the government back for the money they put in your RDSP). If you take money out before you turn 60, you may have to pay the government back. This is because of something called the 10 Year Rule.

If you take any money out of your RDSP before the 10-year waiting period, you will have to pay the government back. You will have to pay $3 for every $1 that is taken out. So, if you took out $1000, you would have to repay the government $3000. This is why you should try to keep your money in your RDSP for at least 10 years.

Inclusion Canada continues to talk to government to change these rules but as of today they remain in place.

You can learn more about taking money out of an RDSP here.

Examples of Maximizing an RDSP

The money can really add up throughout your life. Here is a great example provided by an organization called Partners for Planning (P4P):

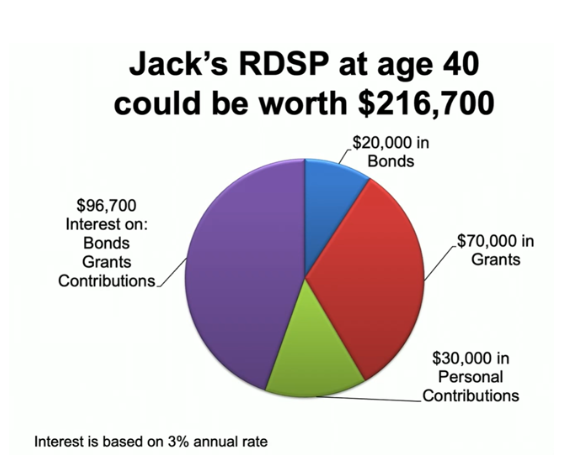

Jack is 10 years old, and his parents open an RDSP for him in 2020. Jack’s parents’ make $16,000 a year. This means Jack can get the full amount of government matching money (called grants and bonds).

His aunt and uncle also put $1,500 into Jack’s RDSP as a gift to him each year until he turns 30. That’s $125 a month.

When Jack turns 19, his own income is then used to determine his eligibility, not his parents. He makes $10,000 a year and because his income is low, can still get the full amount of funding from the government if he continues to put money in.

Question: How much money do you think Jack will have in his RDSP in 2050, when he turns 40 years old, assuming he did not take any money out?

Answer:

Since Jack and his family put $30,000 into his RDSP over the years, by the time Jack is 40 the total amount of money in his RDSP has grown to be $216,700. This increase in money is because of the free money from the government (called grants and bonds) and the extra money Jack made on his money (called interest).

Useful Resources about the Registered Disability Savings Plan (RDSP):

The RDSP can be hard to understand. We have compiled a list of what we think are very helpful places that you can learn more about the RDSP, or get help applying for it. Please take your time and explore the resources on your own below:

- Access RDSP, RDSP Plan Institute

- RDSP Step-by-Step Guide, RDSP Plan Institute

- Guide to the DTC & RDSP for Newcomers with Disabilities, Plan Institute

- RDSP Calculator, Plan Institute

- RDSP Webinars, Plan Institute

- The RDSP Helpsheet, Disability Alliance BC

- Introduction to the RDSP, The P4P Planning Network

- RDSP Webcasts, The P4P Planning Network

- BCANDS, BCANDS offers Indigenous people direct support from RDSP Navigators

We hope you or your family member considers getting an RDSP. We invite you to speak to a financial advisor who may be able to help you figure out and understand if this is right for you.

We encourage everyone to explore this option. Especially because of the free money that the government gives to the RDSP. It is a benefit that everyone should take advantage of.